The bulk and fine chemicals sector is a major user of filtration equipment, making up close to 13% of the global equipment market (and close to 17% of the filter media market). More importantly, it uses probably the widest range of equipment types, and is the largest of all the industrial and commercial sectors as far as the employment of filters in hazardous conditions, and for the processing of aggressive fluids, is concerned. This article reviews the current state of the bulk and fine chemicals sector as a market for filtration and sedimentation equipment, looking especially at those processes using corrosive fluids, or with otherwise hazardous operating conditions.

Sector components

The sector can be split fairly easily into two parts: the manufacture of bulk chemicals and petrochemicals being one, and the other being fine chemicals manufacture, including toiletries and cosmetics. As far as possible, this article covers bulk inorganic and organic chemical manufacture, and fine chemical production, including industrial fermentation, but does not cover pharmaceutical and small-scale biotechnological processing.The key bulk chemicals are made from raw materials occurring naturally on or in the earth, including:• the processing of coal, petroleum and natural gas to give fuel products, organic chemical intermediates and petrochemicals, leading to man-made fibres; nowadays this list is extended to include biological raw materials as the source for many of these same products; • the splitting of air into its main constituents and the recovery of minor components, including carbon dioxide processing;• the manufacture of ceramics and refractory materials, cements, calcium and magnesium compounds, glass, salt, and other sodium and potassium compounds, phosphates and phosphoric acid, all from mineral resources;• the manufacture of sulphuric acid and other sulphur compounds from natural and by-product sulphur;• the manufacture of ammonia from atmospheric nitrogen, and of nitric acid and other nitrogen compounds; and• the manufacture of hydrochloric acid and other halogen compounds; and of a host of other compounds.

It is to be noted that the first component of the above list encompasses the whole of organic chemical processing, while the remainder make up the inorganic products. In all of these chemical production processes, the majority of which are carried out in the liquid phase (and/or with gaseous exhausts), the process use of filtration (and, to a lesser extent, sedimentation) is widely found, as a solid recovery step, or in purifying ingredients, intermediates or final products, and in the recycling or treatment of waste streams.Broadly speaking, bulk chemicals are those used as raw materials in the manufacture of other products, mainly the fine chemicals, which are then sold directly to the domestic or commercial user.(Some fine chemicals are, of course, made from directly from naturally occurring materials, but usually in relatively small quantities). The manufacture of fine chemicals is similarly involved with liquid and gaseous process streams, and hence with filtration.

Aggressive and hazardous processing

The substances that form the raw materials, for the bulk chemicals industry, are all natural materials, which have been on earth for a very long time, and therefore can be assumed, in most of the inorganic processes at least, to be chemically stable (not so for the organic oil and gas materials). It follows that any attempt to extract valuable products from them will require the input of a considerable amount of energy, and, more than likely, some fairly aggressive reaction conditions. This means that the processing equipment, including any filter or centrifuge, must be designed and built, in shape and material, to resist these conditions.The problems that these conditions involve include the physical and chemical nature of the fluid/particle suspension, the nature of the item of equipment and the properties of the environment, both inside the equipment and around it. The nature of the suspension is mainly involved with the corrosive nature of the suspending fluid, usually as a liquid, but gases can be corrosive too. The impact of a suspending gas is more often to do with its temperature, but gaseous corrosion can often be a problem with hot gas filters.Moderately corrosive and/or hot suspensions can be dealt with by using, as filter medium, a temperature resistant polymer, most likely a fluorinated material such as PTFE, in a stainless steel or enamelled steel housing. The filter would need to be protected by a high temperature alarm, to prevent the polymer from being over heated. Rigidised polymeric materials make good media for this level.Stronger corrosive action, or a higher temperature, will need the use of a metal filter medium in a metal housing. For efficient, accurate filtration this will probably mean a multilayer sintered mesh, which can be made into a self-supporting cartridge, over quite a large size range. The sealing of the cartridge into the housing does need careful design in this situation.For the hottest and most aggressive suspensions, it may be necessary to employ ceramic filter media, housed in a high-temperature metal casing. The ceramic medium can be in the form of inverted candles, in rigid form or flexible, or as monolithic blocks carrying a ceramic membrane. Even these materials have upper operating temperature limits, and so need to be protected by an alarm.These filtration systems, here described as aggressive, are also potentially hazardous situations, although the term is usually reserved for systems that, under normal operation, are safe or non-aggressive, but in which an accident can be triggered – by a temperature or pressure excursion, or by excessive reaction. These situations require a very careful survey of potential problems, followed by equally careful design and construction to minimise or eliminate the potential hazard. If a risk still remains, then it would be advisable to mount the system within a building or bunker capable of resisting the worst conceivable accident.A hazard-proof bunker may be used for the filter or centrifuge alone, or for the whole system in which it is set. Other system considerations include:• the use of proper venting, with vent filters to clean any exhaust flow;• where flammable materials are in use, it is as well to consider inert gas blanketing, to separate the process fluids from the surrounding atmosphere; and• reduction in inventory by using smaller processing units (which goes against the effects of larger scale, but may be advisable as a safety precaution) – even micro-reactors and processors may be suitable.However large or small the system, a possible risk must be thoroughly investigated, and a full environmental assessment prepared.

Corporate structure of the chemicals industry

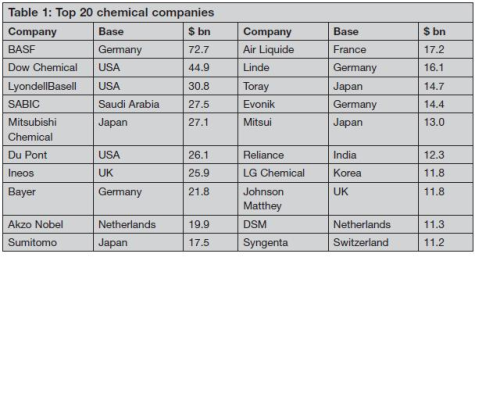

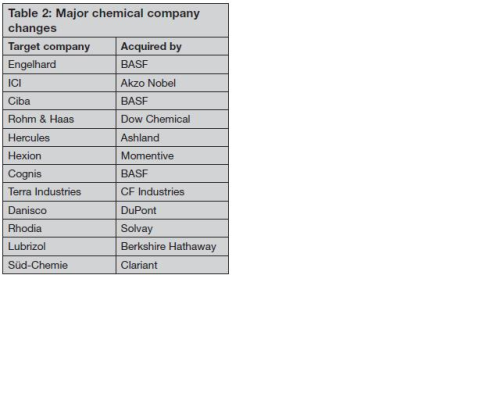

The overall chemicals industry is a complicated one, whose boundaries are not easily drawn in a precise manner. The pharmaceutical and biotechnology components are usually hived off as a separate sector.The bulk and fine chemicals sector contains some very well known companies, the largest of which are listed in Table 1, which shows, for each company, the country in which it is based, and its 2009 turnover in billions of US dollars. On the global scale, there are at least 100 ‘pure’ chemicals manufacturers whose 2009 sales exceeded $2 billion, with the best part of another ten oil and gas companies with sizeable chemical manufacturing divisions.The use of 2009 sales as a comparator has a distorting effect on the order of size in Table 1, because this was the year of maximum impact of the 2008-2010 recession, and some of the listed companies suffered quite marked reductions in turnover for 2009 compared with the peak year of 2007.The boundary definition problem for the chemicals sector is further complicated by the fact that most large energy fuels processing companies also have quite sizeable chemicals businesses. If these companies are included, and they obviously should be, then Table 1 should open up to include Exxon in third position, Shell in fifth, and Total at eleventh.There is also a case, although not quite such a strong one, that can be made for the inclusion of makers of household and personal consumables in the chemicals sector. This would require room to be made in Table 1 for Procter and Gamble, Unilever, L’Oréal, Henkel, Colgate-Palmolive and Reckitt Benckiser, all of whom are of top-20 rank.Finally, there is a somewhat indistinct boundary between bulk chemicals production and mineral processing technologies. Thus the production of pure salt by the extraction of underground rock salt could be regarded as either – but in fact is classed as a mineral production process, as are all processes for the extraction of raw materials from their natural sources, for use in the chemicals sector.As with almost any other industrial sector, the corporate structure of this one has changed significantly over the past few years because of mergers and acquisitions, driven by the emergence of the Asian region (and to a lesser extent South America) as a major supplier, and by the resultant movement of chemical manufacturing activity from Europe and North America to these regions.Some of the more significant M & A activities are listed in Table 2, roughly in chronological order, with the latest last. Some of these were recession driven, and some large companies suffered quite badly – in the top rank of Table 1, LyondellBasell went into Chapter 11 bankruptcy protection, and has only just got out, while Ineos had significant difficulties.

The equipment market

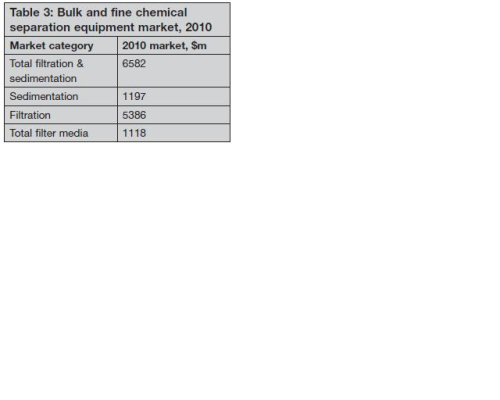

The global equipment market size estimates for the bulk and fine chemicals sector are given in Table 3, firstly as a total filtration and sedimentation equipment figure, which is then split between sedimentation and filtration equipment. These figures are supplemented with a separate estimate for filter media sales. The estimates are quoted for 2010, in millions of US dollars, at the mid-year average currency value. The equipment estimates in Table 3 only include that ancillary equipment (such as drive motors) necessary for its safe operation.The filtration equipment total in Table 3 is 12.7% of the total global filtration figure (and that for filter media is 16.9%). The sector filtration equipment total is estimated to be split into $4190 millions for bulk chemical processing and $1196 millions for fine chemicals. The sector market will not grow as fast as that for pharmaceutical chemicals manufacture, and compound annual growth figures are expected to average 5.4% for the five years to 2015 for the whole sector, with corresponding component growth rates of 4.8% for bulk chemicals and petrochemicals, and 5.9% for fine chemicals.

The future

It is relatively easy to forecast the trends of the near future for the bulk and fine chemicals industry: the driving forces currently causing change will continue to do so:• end-user demand for finer degrees of filtration, which will accelerate the spread of membrane usage in all materials, but especially inorganics ;• need to achieve higher energy efficiencies (both because of the rapidly rising cost of energy, and to minimise carbon footprints);• more stringent application of health and safety regulations, especially in the cleaning of exhaust gases, and the ensuring of process safety;• more stringent environmental regulations, especially imposing an increased need for waste material recycle (already being anticipated in the form of ‘green chemistry’);• the ability to filter hotter liquid suspensions; and• the rapid growth of process use of biomass, primarily of vegetable origin and especially food product wastes, as fuel, and, more importantly, as a source of the chemicals now made from petrochemical sources.

The filter, and to a lesser extent, the centrifuge, have a very important role in these trends, which are all giving rise to an increase in use and hence in market size. Aggressive processing needs are a common feature of many active market drivers.The picture is not entirely rosy: the economic climate is not encouraging, and investment funds will be hard to come by for a while; there is no halting the movement of production capacity east and south, in search of cheaper energy and labour. This will depress those developed areas away from which the movement is occurring, but it will not be long before the emerging countries will more than make up for the shortfall, the BRIC countries, South Africa, and Indonesia especially. ’Chemical’ is still a dirty word in the public conception (although not as dirty as ‘nuclear’), and this view may not be reversed until too late.It is rather less easy to foresee the long term trends. A suggested list would include the following:• a return to favour of nuclear power, one of the most strongly aggressive and hazardous of environments – a change that is constantly being urged, but with little action, and that largely suspended since the events at Fukushima;• the demonstration of a successful method of carbon capture and sequestration, followed by its rapid implementation at stationary generation sites;• extending from that, a practically possible and economically viable process for stripping ambient air of carbon dioxide – in parallel, perhaps, with new processes for converting the carbon dioxide to other carbon chemicals;• the successful development of carbon nanoparticle technology;• a less energy demanding (which probably means bacteria driven) conversion of atmospheric nitrogen into a usable chemical;• the rapid arrival as an economic process of the ‘second generation’ of biomass using non-food crops or food production wastes, to make the dream of a biorefinery a reality;• the creation of a range of processes, especially in pharmaceutical and fine chemical production, based on enzymic catalysis; and• the development of an artificial photosynthesis process, to create energy directly from sunlight (and consume carbon dioxide on the way).